https://prosperitythinkers.com/personal-finance/three-monkeys-and-cat-pick-stocks/

This article will be the topic for today’s post.

Returning again to the wisdom of Burton Malkiel, who was the subject of our last article, we find this sage of finance being quoted as stating,

“A blindfolded monkey throwing darts at a newspaper’s financial pages could select a portfolio that would do just as well as one carefully selected by experts.”

It would seem that some researchers took this quote a bit too literally as the article suggests, and decided to perform variations of the above described experiment.

The article discusses these contests of stock picking in detail. As apparently, in different instances, a cat, school children, and dart throwers, were employed to discern differing investment portfolios. In each instance described, the seemingly random selection of equities, regardless of the employed methodologies, outperformed both actively managed funds, and broad indexes.

I decided to perform my own trial research as it relates to this sort investment approach.

#### WARNING – INVESTMENT OF ANY SORT BEARS RISK! THIS ARTICLE IS NOT FINANCIAL ADVICE! DO NOT REPLICATE THIS EXPERIMENT AND EXPECT TO MAKE MONEY! ####

First, I chose a few financial benchmarks.

AI Powered Equity ETF (AIEQ) – An ETF which is described as, “AIEQ uses artificial intelligence to analyze and identify US stocks believed to have the highest probability of capital appreciation over the next 12 months, while exhibiting volatility similar to the overall US market. The fund selects 30 to 125 constituents and has no restrictions on the market cap of its included securities. The model suggests weights based on capital appreciation potential and correlation to other included companies, subject to a 10% cap per holding. It is worth noting that while AIEQ relies heavily on its quantitative model, the fund is actively-managed, and follows no index.”

Source: https://www.etf.com/AIEQ

Fidelity Magellan Fund (FMAGX) – A famous actively managed mutual fund which possess the following strategy, “The Fund seeks capital appreciation. Fidelity Management & Research may buy "growth" stocks or "value" stocks or a combination of both. They rely on fundamental analysis of each issuer and its potential for success in light of its current financial condition, its industry position, and economic and market conditions.”

Source: https://www.marketwatch.com/investing/fund/fmagx

Vanguard Total Stock Market Index Fund (VTSAX) – Description provided, “Created in 1992, Vanguard Total Stock Market Index Fund is designed to provide investors with exposure to the entire U.S. equity market, including small-, mid-, and large-cap growth and value stocks. The fund’s key attributes are its low costs, broad diversification, and the potential for tax efficiency. Investors looking for a low-cost way to gain broad exposure to the U.S. stock market who are willing to accept the volatility that comes with stock market investing may wish to consider this fund as either a core equity holding or your only domestic stock fund.”

Source: https://investor.vanguard.com/investment-products/mutual-funds/profile/vtsax

With these benchmarks defined, I set off too to create my own randomly established equity fund. To fairly decide which equities my fund would hold, I utilized the two websites:

https://www.rayberger.org/random-stock-picker/

~AND~

https://www.randstock.ca/selector

The only equity selections which I outright rejected from inclusion were fixed income ETFs, and ETFs which sought to replicate the performance of a commodity.

All funds would receive an equal allocations of capital ($ 1000), and the initial issue price of my Random Fund would be set at $ 10.00 a share.

Oshkosh Corporation (OSK) - Oshkosh Corporation designs, manufacture, and markets specialty trucks and access equipment vehicles worldwide. Sector(s): Industrials

Franklin FTSE Brazil ETF (FLBR) - The FTSE Brazil Capped Index is based on the FTSE Brazil Index and is designed to measure the performance of Brazilian large- and mid-capitalization stocks. Sector(s): ETF

Public Storage (PSA) - Public Storage, a member of the S&P 500 and FT Global 500, is a REIT that primarily acquires, develops, owns, and operates self-storage facilities. Sector(s) - Real Estate

Dorian LPG Ltd. (LPG) - Dorian LPG Ltd., together with its subsidiaries, engages in the transportation of liquefied petroleum gas (LPG) through its LPG tankers worldwide. The company owns and operates very large gas carriers (VLGCs). Sector(s) - Energy

Delta Air Lines, Inc. (DAL) - Delta Air Lines, Inc. provides scheduled air transportation for passengers and cargo in the United States and internationally. Sector(s) – Industrials

Grupo Industrial Saltillo, S.A.B. de C.V. (SALT) (MX) - Grupo Industrial Saltillo, S.A.B. de C.V. engages in the design, manufacture, wholesale, and marketing of products for automotive, construction, and houseware industries in Mexico, Europe, and Asia. Sector(s) - Consumer Cyclical

Equity LifeStyle Properties, Inc. (ELS) - We are a self-administered, self-managed real estate investment trust (REIT) with headquarters in Chicago. Sector(s) – Real Estate

SPDR Portfolio S&P 500 ETF (SPLG) - Under normal market conditions, the fund generally invests substantially all, but at least 80%, of its total assets in the securities comprising the index. Sector(s) – ETF

DHT Holdings, Inc. (DHT) - DHT Holdings, Inc., through its subsidiaries, owns and operates crude oil tankers primarily in Monaco, Singapore, and Norway. As of March 16, 2023, it had a fleet of 23 very large crude carriers. Sector(s) - Energy

Norfolk Southern Corporation (NSC) - Norfolk Southern Corporation, together with its subsidiaries, engages in the rail transportation of raw materials, intermediate products, and finished goods in the United States. Sector(s) – Industrials

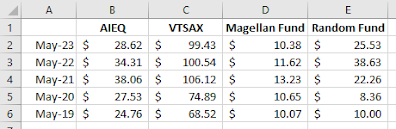

With a purchase date of each equity being set at 5/1/2019 (closing price), our fictitious Random Fund performed as shown below:

https://www.randstock.ca/selector

The only equity selections which I outright rejected from inclusion were fixed income ETFs, and ETFs which sought to replicate the performance of a commodity.

All funds would receive an equal allocations of capital ($ 1000), and the initial issue price of my Random Fund would be set at $ 10.00 a share.

Oshkosh Corporation (OSK) - Oshkosh Corporation designs, manufacture, and markets specialty trucks and access equipment vehicles worldwide. Sector(s): Industrials

Franklin FTSE Brazil ETF (FLBR) - The FTSE Brazil Capped Index is based on the FTSE Brazil Index and is designed to measure the performance of Brazilian large- and mid-capitalization stocks. Sector(s): ETF

Public Storage (PSA) - Public Storage, a member of the S&P 500 and FT Global 500, is a REIT that primarily acquires, develops, owns, and operates self-storage facilities. Sector(s) - Real Estate

Dorian LPG Ltd. (LPG) - Dorian LPG Ltd., together with its subsidiaries, engages in the transportation of liquefied petroleum gas (LPG) through its LPG tankers worldwide. The company owns and operates very large gas carriers (VLGCs). Sector(s) - Energy

Delta Air Lines, Inc. (DAL) - Delta Air Lines, Inc. provides scheduled air transportation for passengers and cargo in the United States and internationally. Sector(s) – Industrials

Grupo Industrial Saltillo, S.A.B. de C.V. (SALT) (MX) - Grupo Industrial Saltillo, S.A.B. de C.V. engages in the design, manufacture, wholesale, and marketing of products for automotive, construction, and houseware industries in Mexico, Europe, and Asia. Sector(s) - Consumer Cyclical

Equity LifeStyle Properties, Inc. (ELS) - We are a self-administered, self-managed real estate investment trust (REIT) with headquarters in Chicago. Sector(s) – Real Estate

SPDR Portfolio S&P 500 ETF (SPLG) - Under normal market conditions, the fund generally invests substantially all, but at least 80%, of its total assets in the securities comprising the index. Sector(s) – ETF

DHT Holdings, Inc. (DHT) - DHT Holdings, Inc., through its subsidiaries, owns and operates crude oil tankers primarily in Monaco, Singapore, and Norway. As of March 16, 2023, it had a fleet of 23 very large crude carriers. Sector(s) - Energy

Norfolk Southern Corporation (NSC) - Norfolk Southern Corporation, together with its subsidiaries, engages in the rail transportation of raw materials, intermediate products, and finished goods in the United States. Sector(s) – Industrials

With a purchase date of each equity being set at 5/1/2019 (closing price), our fictitious Random Fund performed as shown below:

Now let’s compare the fund’s performance against our previously decided upon benchmarks:

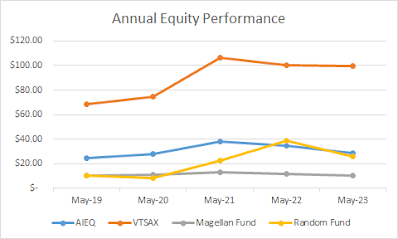

Graphing the performance of each fund across multiple years:

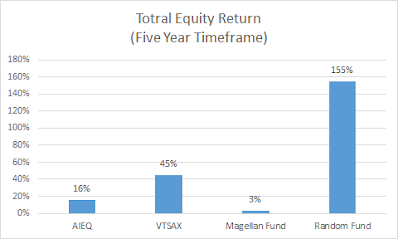

Or looking at returns over the span of a five year period:

Strangely enough, our Random Fund outperforms the advisor managed fund (Magellan Fund), the broad based index fund (VTSAX), and the AI managed fund (AIEQ). While actively managed funds typically underperform index benchmarks for a multitude of reasons, I found it incredibly odd that my e-monkey Random Fund outperformed even the index itself. This is also what happened to be the case in the similarly conducted experiments mentioned within the article.

Let’s think of a few informed reasons as to why this might be:

1. Actively managed funds often turn over equities with far greater frequency when compared to their index counterparts. Index funds typically owe the majority of their equity turnover to modifications made to the underlying index. This causes both tax implications, and a lack of dividend opportunities.

2. Our Random Fund contains less components, and is less balanced than its competitors. Therefore, we would expect the fund to be more generally impacted by variance. In bull markets, I would expect such a selection of equities to outperform an underlying index. However, in bear markets, the inverse should hold true. In that, our Random Fund would likely lose more value than its contemporaries.

3. The time frame which is being utilized to assess performance is both short in duration and directionally positive for equities.

4. Actively managed funds attempt to protect investors from downside, which also limits the upside potential for returns.

5. As it relates to #5, actively managed funds must also keep greater amounts of cash and cash equivalents on hand. This equates to time out of the market.

6. Actively managed funds have higher management fees, which are utilized to compensate fund managers.

7. Index components are themselves, popular equities. This means that incoming investment money either chases the price of individual equites upward through individual stock purchase, or through periodic fund purchases.

8. Randomly selecting equities is far less biased than making an “informed selection”. Such bias often manifests in vastly over-estimating ones abilities, and under-assessing the abilities of others. Such an over estimation may cause an individual manager to go overweight in a particular sector or individual equity, and in doing such, miss opportunities elsewhere. As indexes are broad, there is always the exposure to opportunity within a bull market. This combined with the other previously numbered aspects, likely partially explains the underperformance of actively managed funds.

9. As it relates to point #9. In a bull market, over a short time span, randomly selecting a small number of equities may be the best method to employing a strategy which beats alpha. As bias will be eliminated, and beta will be increased.

10. Active fund managers may not possess the fiduciary ability to allow their investment strategies to materialize. As the annual alpha is always the metric which high net worth clients measure all performance against, an informed, but otherwise risk incurring position must deliver results in the intermediate term, or risk liquidation at a loss in both capital and opportunity.

Graphing the performance of each fund across multiple years:

Or looking at returns over the span of a five year period:

Strangely enough, our Random Fund outperforms the advisor managed fund (Magellan Fund), the broad based index fund (VTSAX), and the AI managed fund (AIEQ). While actively managed funds typically underperform index benchmarks for a multitude of reasons, I found it incredibly odd that my e-monkey Random Fund outperformed even the index itself. This is also what happened to be the case in the similarly conducted experiments mentioned within the article.

Let’s think of a few informed reasons as to why this might be:

1. Actively managed funds often turn over equities with far greater frequency when compared to their index counterparts. Index funds typically owe the majority of their equity turnover to modifications made to the underlying index. This causes both tax implications, and a lack of dividend opportunities.

2. Our Random Fund contains less components, and is less balanced than its competitors. Therefore, we would expect the fund to be more generally impacted by variance. In bull markets, I would expect such a selection of equities to outperform an underlying index. However, in bear markets, the inverse should hold true. In that, our Random Fund would likely lose more value than its contemporaries.

3. The time frame which is being utilized to assess performance is both short in duration and directionally positive for equities.

4. Actively managed funds attempt to protect investors from downside, which also limits the upside potential for returns.

5. As it relates to #5, actively managed funds must also keep greater amounts of cash and cash equivalents on hand. This equates to time out of the market.

6. Actively managed funds have higher management fees, which are utilized to compensate fund managers.

7. Index components are themselves, popular equities. This means that incoming investment money either chases the price of individual equites upward through individual stock purchase, or through periodic fund purchases.

8. Randomly selecting equities is far less biased than making an “informed selection”. Such bias often manifests in vastly over-estimating ones abilities, and under-assessing the abilities of others. Such an over estimation may cause an individual manager to go overweight in a particular sector or individual equity, and in doing such, miss opportunities elsewhere. As indexes are broad, there is always the exposure to opportunity within a bull market. This combined with the other previously numbered aspects, likely partially explains the underperformance of actively managed funds.

9. As it relates to point #9. In a bull market, over a short time span, randomly selecting a small number of equities may be the best method to employing a strategy which beats alpha. As bias will be eliminated, and beta will be increased.

10. Active fund managers may not possess the fiduciary ability to allow their investment strategies to materialize. As the annual alpha is always the metric which high net worth clients measure all performance against, an informed, but otherwise risk incurring position must deliver results in the intermediate term, or risk liquidation at a loss in both capital and opportunity.

That's all for today.

Until next time, stay curious data heads!

-RD