Following up on the prior article, a reader of this site wrote to me and asked (paraphrasing):

“I really enjoyed your last entry as it pertains to randomly selected portfolios. However, I remain skeptical. How would another random selection of stocks perform within a historical bear market? Also, how would these stocks perform across a longer duration of time?”

Great questions! We would not be scientists if we didn’t attempt to replicate our results!

We’ll start with a new list of random equities. The same rules apply. No commodity funds or bond funds will be included within our Random Portfolio. We will be going back to the late 1990’s, to the zenith of the dot com bubble, and then into the lethargy of the early 2000’s. This experiment will be imperfect, as amongst other confounding factors, our random stock picker can only pick from equities which are still public, and still in existence. Any equity which did not make it to the present, unfortunately, cannot be included within our experiment.

#### WARNING – INVESTMENT OF ANY SORT BEARS RISK! THIS ARTICLE IS NOT FINANCIAL ADVICE! DO NOT REPLICATE THIS EXPERIMENT AND EXPECT TO MAKE MONEY! ####

To fairly decide as to which equities our fund would hold, I utilized the websites:

https://www.rayberger.org/random-stock-picker/

~AND~

https://www.randstock.ca/selector

So, let’s meet our new components:

Fair Isaac Corporation (FICO) - Fair Isaac Corporation develops analytic, software, and data decisioning technologies and services that enable businesses to automate, enhance, and connect decisions in the Americas, Europe, the Middle East, Africa, and the Asia Pacific. Sector(s): Technology

Par Technology Corporation (PAR) - PAR Technology Corporation, together with its subsidiaries, provides technology solutions to the restaurant and retail industries worldwide. Sector(s): Software Application

IMAX Corporation (IMAX) - IMAX Corporation, together with its subsidiaries, operates as a technology platform for entertainment and events worldwide. Sector(s): Communication Services

Spectrum Brands Holdings, Inc. (SPB) - Spectrum Brands Holdings, Inc. operates as a branded consumer products company worldwide. It operates through three segments: Home and Personal Care; Global Pet Care; and Home and Garden. Sector(s): Consumer Defensive

Patterson Companies, Inc. (PDCO) - Patterson Companies, Inc. engages in distribution of dental and animal health products in the United States, the United Kingdom, and Canada. Sector(s): Healthcare

The Walt Disney Company (DIS) - The Walt Disney Company, together with its subsidiaries, operates as an entertainment company worldwide. Sector(s): Communication Services

Regis Corporation (RGS) - Regis Corporation owns, operates, and franchises hairstyling and hair care salons in the United States, Canada, Puerto Rico, and the United Kingdom. Sector(s): Consumer Cyclical

Synovus Financial Corp (SNV) - Synovus Financial Corp. operates as the bank holding company for Synovus Bank that provides commercial and consumer banking products and services. Sector(s): Financial Services

Royal Bank of Canada (RY) - Royal Bank of Canada operates as a diversified financial service company worldwide. Sector(s): Financial Services

Incyte Corporation (INCY) - Incyte Corporation, a biopharmaceutical company, engages in the discovery, development, and commercialization of therapeutics for hematology/oncology, and inflammation and autoimmunity areas in the United States, Europe, Japan, and internationally. Sector(s): Healthcare

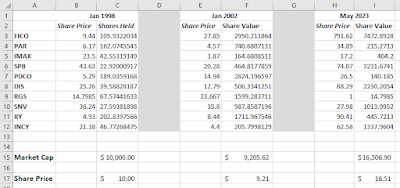

With a purchase date of each equity being set at 1/1/1998 (closing price), our fictitious Random Fund performs as shown below:

Again, I choose a few benchmarks to compare this performance against:

Fidelity Magellan Fund (FMAGX) – A famous actively managed mutual fund which possess the following strategy, “The Fund seeks capital appreciation. Fidelity Management & Research may buy "growth" stocks or "value" stocks or a combination of both. They rely on fundamental analysis of each issuer and its potential for success in light of its current financial condition, its industry position, and economic and market conditions.”

Source: https://www.marketwatch.com/investing/fund/fmagx

Vanguard Total Stock Market Index Fund (VTSAX) – Description provided, “Created in 1992, Vanguard Total Stock Market Index Fund is designed to provide investors with exposure to the entire U.S. equity market, including small-, mid-, and large-cap growth and value stocks. The fund’s key attributes are its low costs, broad diversification, and the potential for tax efficiency. Investors looking for a low-cost way to gain broad exposure to the U.S. stock market who are willing to accept the volatility that comes with stock market investing may wish to consider this fund as either a core equity holding or your only domestic stock fund.”

Source: https://investor.vanguard.com/investment-products/mutual-funds/profile/vtsax

### And Introducing a New Challenger! ###

Columbia Seligman Technology & Info Fd;A (SLMCX) – “The Fund seeks to provide shareholders with capital gain. The Fund will invest at least 80% of its net assets in securities of companies operating in the communications, information and related industries, including companies operating in the information technology and telecommunications sectors.”

Source: https://www.marketwatch.com/investing/fund/slmcx

Why (SLMCX) and not the previous competitive benchmark (AIEQ)?

As the AI Powered Equity ETF (AIEQ) did not exist in the 1990’s, I decided to select a fund which is managed by a company which once employed Charles Kadlec. Who is Charles Kadlec? He is an author and financier, having written the book: Dow 100,000: Fact or Fiction.

Dow 100,000: Fact or Fiction was released in September 1999, having likely been composed throughout 1998. So, in the spirit of the technical optimism which existed from that era, and which still exists within the hearts of AIEQ investors, I choose the Columbia Seligman Technology and Information Fund Class A (SLMCX) as our final benchmark.

First, let’s consider our returns over the span of a five year period:

-RD

“I really enjoyed your last entry as it pertains to randomly selected portfolios. However, I remain skeptical. How would another random selection of stocks perform within a historical bear market? Also, how would these stocks perform across a longer duration of time?”

Great questions! We would not be scientists if we didn’t attempt to replicate our results!

We’ll start with a new list of random equities. The same rules apply. No commodity funds or bond funds will be included within our Random Portfolio. We will be going back to the late 1990’s, to the zenith of the dot com bubble, and then into the lethargy of the early 2000’s. This experiment will be imperfect, as amongst other confounding factors, our random stock picker can only pick from equities which are still public, and still in existence. Any equity which did not make it to the present, unfortunately, cannot be included within our experiment.

#### WARNING – INVESTMENT OF ANY SORT BEARS RISK! THIS ARTICLE IS NOT FINANCIAL ADVICE! DO NOT REPLICATE THIS EXPERIMENT AND EXPECT TO MAKE MONEY! ####

To fairly decide as to which equities our fund would hold, I utilized the websites:

https://www.rayberger.org/random-stock-picker/

~AND~

https://www.randstock.ca/selector

So, let’s meet our new components:

Fair Isaac Corporation (FICO) - Fair Isaac Corporation develops analytic, software, and data decisioning technologies and services that enable businesses to automate, enhance, and connect decisions in the Americas, Europe, the Middle East, Africa, and the Asia Pacific. Sector(s): Technology

Par Technology Corporation (PAR) - PAR Technology Corporation, together with its subsidiaries, provides technology solutions to the restaurant and retail industries worldwide. Sector(s): Software Application

IMAX Corporation (IMAX) - IMAX Corporation, together with its subsidiaries, operates as a technology platform for entertainment and events worldwide. Sector(s): Communication Services

Spectrum Brands Holdings, Inc. (SPB) - Spectrum Brands Holdings, Inc. operates as a branded consumer products company worldwide. It operates through three segments: Home and Personal Care; Global Pet Care; and Home and Garden. Sector(s): Consumer Defensive

Patterson Companies, Inc. (PDCO) - Patterson Companies, Inc. engages in distribution of dental and animal health products in the United States, the United Kingdom, and Canada. Sector(s): Healthcare

The Walt Disney Company (DIS) - The Walt Disney Company, together with its subsidiaries, operates as an entertainment company worldwide. Sector(s): Communication Services

Regis Corporation (RGS) - Regis Corporation owns, operates, and franchises hairstyling and hair care salons in the United States, Canada, Puerto Rico, and the United Kingdom. Sector(s): Consumer Cyclical

Synovus Financial Corp (SNV) - Synovus Financial Corp. operates as the bank holding company for Synovus Bank that provides commercial and consumer banking products and services. Sector(s): Financial Services

Royal Bank of Canada (RY) - Royal Bank of Canada operates as a diversified financial service company worldwide. Sector(s): Financial Services

Incyte Corporation (INCY) - Incyte Corporation, a biopharmaceutical company, engages in the discovery, development, and commercialization of therapeutics for hematology/oncology, and inflammation and autoimmunity areas in the United States, Europe, Japan, and internationally. Sector(s): Healthcare

With a purchase date of each equity being set at 1/1/1998 (closing price), our fictitious Random Fund performs as shown below:

Again, I choose a few benchmarks to compare this performance against:

Fidelity Magellan Fund (FMAGX) – A famous actively managed mutual fund which possess the following strategy, “The Fund seeks capital appreciation. Fidelity Management & Research may buy "growth" stocks or "value" stocks or a combination of both. They rely on fundamental analysis of each issuer and its potential for success in light of its current financial condition, its industry position, and economic and market conditions.”

Source: https://www.marketwatch.com/investing/fund/fmagx

Vanguard Total Stock Market Index Fund (VTSAX) – Description provided, “Created in 1992, Vanguard Total Stock Market Index Fund is designed to provide investors with exposure to the entire U.S. equity market, including small-, mid-, and large-cap growth and value stocks. The fund’s key attributes are its low costs, broad diversification, and the potential for tax efficiency. Investors looking for a low-cost way to gain broad exposure to the U.S. stock market who are willing to accept the volatility that comes with stock market investing may wish to consider this fund as either a core equity holding or your only domestic stock fund.”

Source: https://investor.vanguard.com/investment-products/mutual-funds/profile/vtsax

### And Introducing a New Challenger! ###

Columbia Seligman Technology & Info Fd;A (SLMCX) – “The Fund seeks to provide shareholders with capital gain. The Fund will invest at least 80% of its net assets in securities of companies operating in the communications, information and related industries, including companies operating in the information technology and telecommunications sectors.”

Source: https://www.marketwatch.com/investing/fund/slmcx

Why (SLMCX) and not the previous competitive benchmark (AIEQ)?

As the AI Powered Equity ETF (AIEQ) did not exist in the 1990’s, I decided to select a fund which is managed by a company which once employed Charles Kadlec. Who is Charles Kadlec? He is an author and financier, having written the book: Dow 100,000: Fact or Fiction.

Dow 100,000: Fact or Fiction was released in September 1999, having likely been composed throughout 1998. So, in the spirit of the technical optimism which existed from that era, and which still exists within the hearts of AIEQ investors, I choose the Columbia Seligman Technology and Information Fund Class A (SLMCX) as our final benchmark.

First, let’s consider our returns over the span of a five year period:

As was mentioned within the prior article, we should typically expect actively managed funds to hold together more consistently throughout market downturns. In this case, the downturn was the collapse of the tech-bubble.

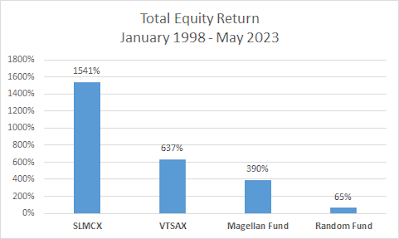

As we stretch our assessment period out to the present, our returns are as follows:

Over a larger period of time, our poor Random Fund got clobbered. The total stock market index fund outperformed the actively managed fund – Magellan. However, in this instance, the (managed) tech sector heavy SLMCX fund destroyed all competitors.

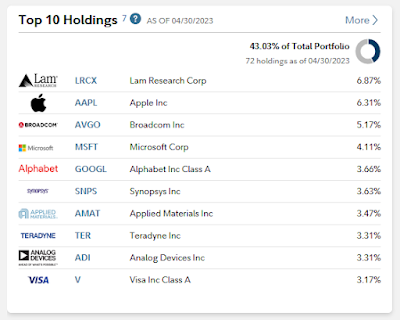

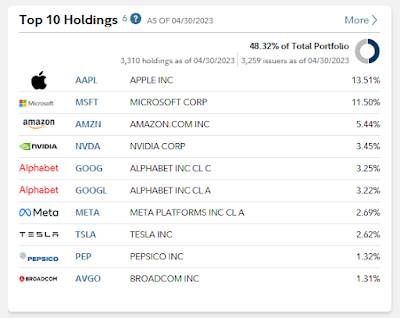

Let’s take a look at the top holdings of the well performing SLMCX:

This mix heavily resembles the top holdings of Fidelity’s NASDAQ Composite Index Fund:

However, SLMCX is a bit heavier in chip sector allocation.

Though the gains of SLMCX are impressive in comparison, it would appear that SLMCX's composition is mostly derived from the NASDAQ composite. When compared against the broad US index, SLMCX is a stud. When compared against the NASDAQ composite over a 5-year period, SLMCX underperforms.

Why?

As it pertains to the SLMCX and the NASDAQ both trouncing their competition, it might have something to do with the composition of US markets.

For the past few decades, the US technology sector has benefitted from both a lax regulatory environment, and significant taxpayer investment. National Defense spending allocations often find their way into tech sector contracts. Research grant money and public infrastructure investments also helps drive rapid growth.

Random Fund melted on the pavement in comparison to both its index and managed counterparts, most likely due to its holdings not being predominately comprised of composite components.

Managed funds are forced to dink and dunk, spending more time out of the market than their index counterparts. These transactions cause taxes and other costs to be assessed. There is also the management fee. Composites themselves are almost a self-fulfilling prophecy. Stocks included within a composite appreciate in value when funds which benchmark the composite are purchased. The stocks themselves also can be purchased individually, which further drives mutual appreciation.

Over a larger period of time, our poor Random Fund got clobbered. The total stock market index fund outperformed the actively managed fund – Magellan. However, in this instance, the (managed) tech sector heavy SLMCX fund destroyed all competitors.

Let’s take a look at the top holdings of the well performing SLMCX:

This mix heavily resembles the top holdings of Fidelity’s NASDAQ Composite Index Fund:

However, SLMCX is a bit heavier in chip sector allocation.

Though the gains of SLMCX are impressive in comparison, it would appear that SLMCX's composition is mostly derived from the NASDAQ composite. When compared against the broad US index, SLMCX is a stud. When compared against the NASDAQ composite over a 5-year period, SLMCX underperforms.

Why?

As it pertains to the SLMCX and the NASDAQ both trouncing their competition, it might have something to do with the composition of US markets.

For the past few decades, the US technology sector has benefitted from both a lax regulatory environment, and significant taxpayer investment. National Defense spending allocations often find their way into tech sector contracts. Research grant money and public infrastructure investments also helps drive rapid growth.

Random Fund melted on the pavement in comparison to both its index and managed counterparts, most likely due to its holdings not being predominately comprised of composite components.

Managed funds are forced to dink and dunk, spending more time out of the market than their index counterparts. These transactions cause taxes and other costs to be assessed. There is also the management fee. Composites themselves are almost a self-fulfilling prophecy. Stocks included within a composite appreciate in value when funds which benchmark the composite are purchased. The stocks themselves also can be purchased individually, which further drives mutual appreciation.

So why do investors even consider actively managed funds / hedge funds as investment options?

1. Diversification. Typically, wealthier individuals prefer to very broadly diversify their capital allocation. To assist in achieving aspects of an individualized allocation strategy, managed funds offer the opportunity to seek out alternative or exotic investments.

2. Liquidity. As most financial crises, both individual and societal, are caused by liquidity contractions, investors with excess capital who are savvy, may want to maintain both excess liquidity and market exposure at the cost of potential sub-alpha returns. This offset is accepted for the sake of liquidity access in times of financial uncertainty.

3. Financial Planning. Financial advisors can assist in personal financial guidance and estate planning. In some instances, the advisor relationship entails that the advisee be invested in financial products provided by the advisor's firm. These funds, while sometimes bearing a premium, may assist the client in maintaining the above listed attributes. This is achieved while also providing the client with a personalized financial plan.

That is it for this article.

I'll see you next week!